Exploring the Landscape of Contemporary Issues in Banking

Document from University about Exploring Landscape of Contemporary Issues. The Pdf provides a clear overview of economic and macroeconomic challenges, technological advancements like AI and ML, and regulatory pressures in the banking sector. This University level Economics material is structured for quick review.

See more63 Pages

Unlock the full PDF for free

Sign up to get full access to the document and start transforming it with AI.

Preview

EXPLORING LANDSCAPE OF CONTEMPORARY ISSUES

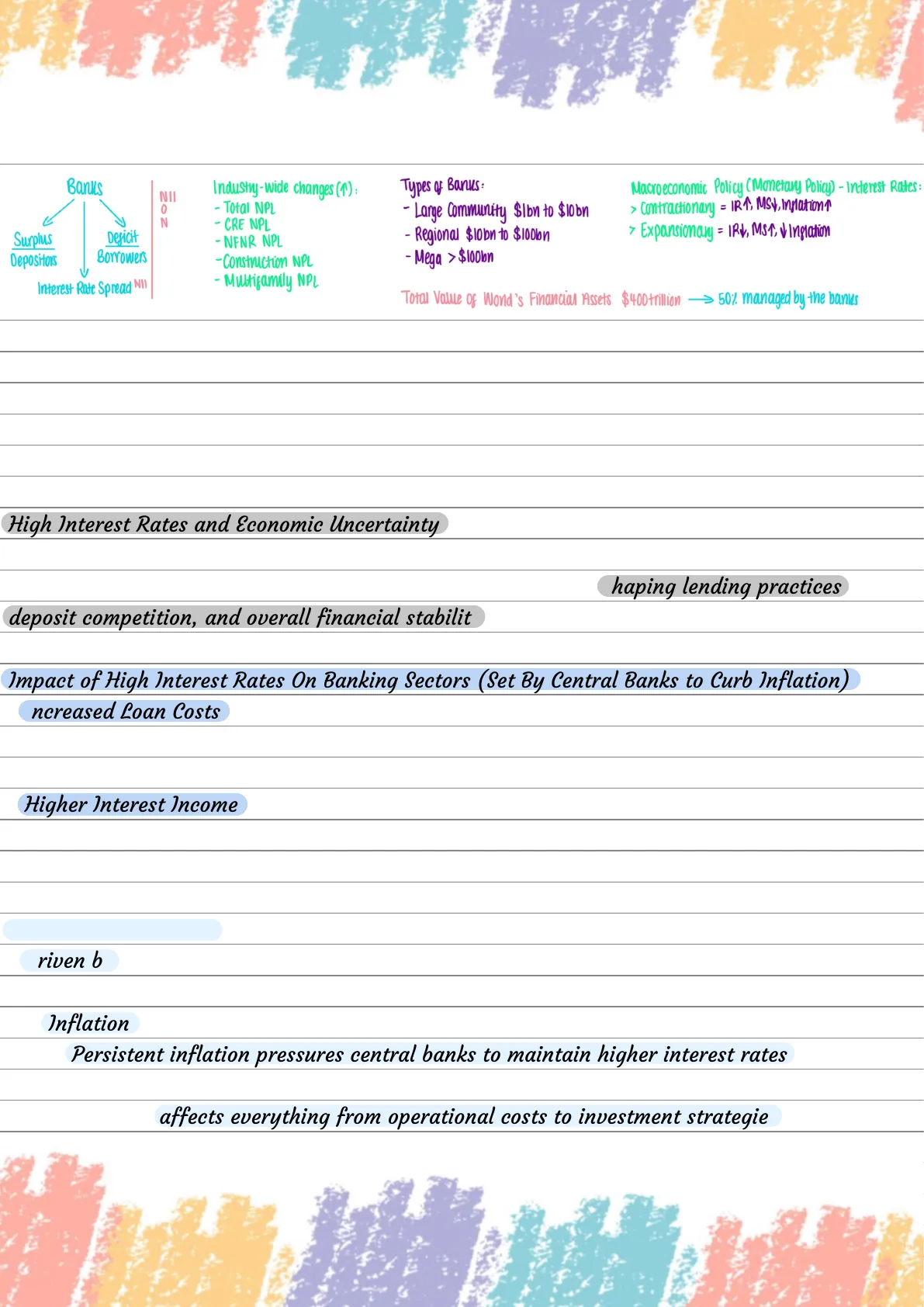

Banks

NII

0

N

Surplus

Depositors

Deficit

Borrowers

Interest Rate Spread NI!

Industry-wide Changes

- Total NPL

- CRE NPL

- NENR NPL

- Construction NPL

- Multifamily NPL

Types of Banks

- Large Community $Ibn to $10 bn

- Regional $10 bn to $100bn

- Mega > $100bn

Macroeconomic Policy (Monetary Policy) - Interest Rates

- contractionary = IR1; MSV, Inflation1

- Expansionary = IRV, MST, V Inflation

Total Value of World's Financial Assets $400 trillion -> 50% managed by the banks

NPL = Non-Performing Loan

CRE = Commercial Real Estate

NFNR = Non Farm Non Residential

ECONOMIC AND MACROECONOMIC CHALLENGES

High Interest Rates and Economic Uncertainty

Global economy and banking sector is affected by high interest rates and macroeconomic

factors, especially during periods of significant uncertainty - shaping lending practices,

deposit competition, and overall financial stability

Impact of High Interest Rates On Banking Sectors (Set By Central Banks to Curb Inflation)

- Increased Loan Costs: raise the cost of borrowing for consumers and businesses -> reduced

demand for loans and refinancing -> slows down the growth of banks' lending portfolios and

affect their profitability - Higher Interest Income: banks can earn more from the interest on loans -> this benefit is

often offset by the increased cost of deposits and other funding sources - Increase In Interest Rates = Increase In Mortgage

Economic Uncertainty

Driven by factors such as geopolitical tensions, supply chain disruptions, and the lingering

effects of the COVID-19 pandemic, poses additional challenges:

- Inflation:

Persistent inflation pressures central banks to maintain higher interest rates, which

further complicates the economic landscape for banks

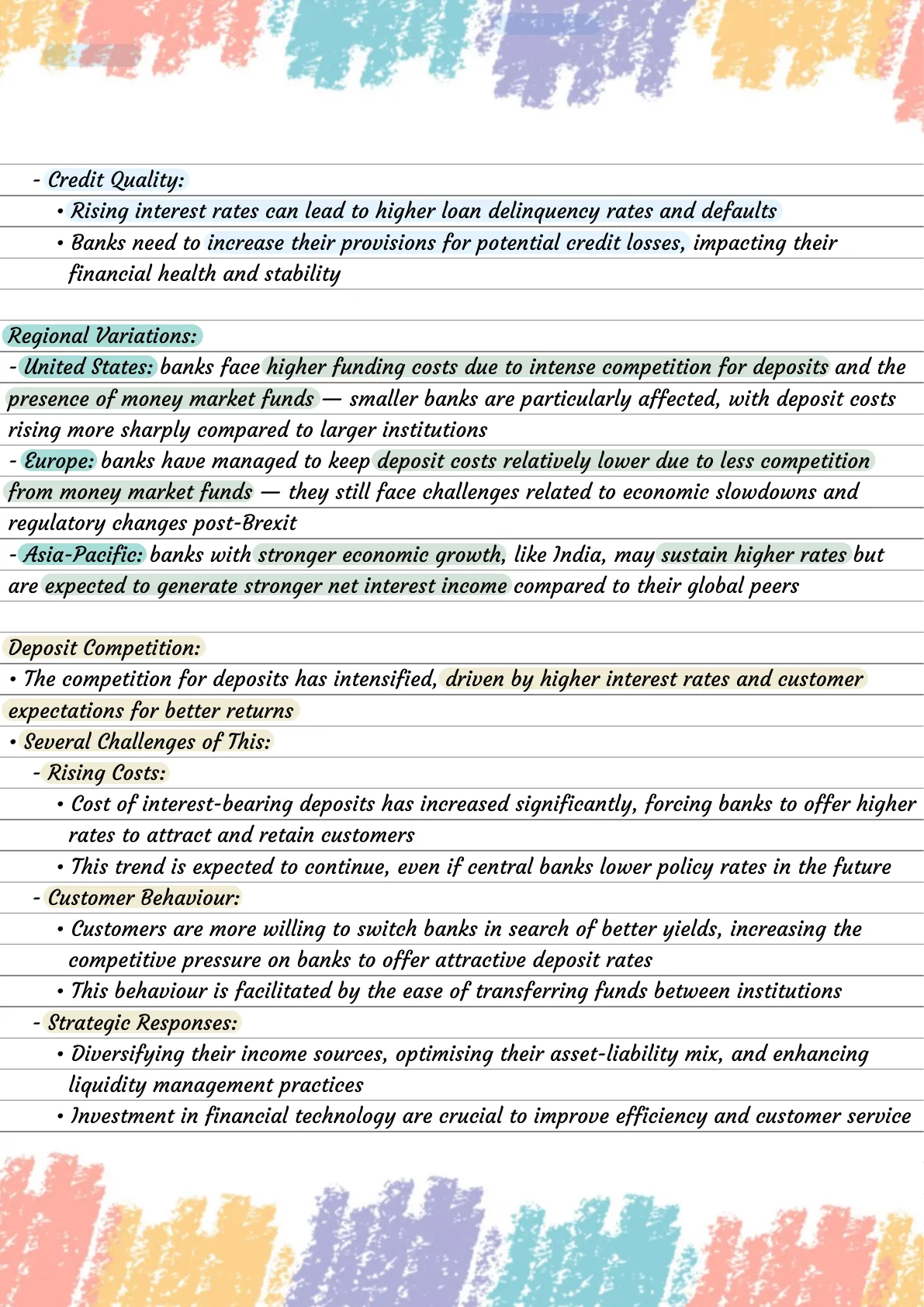

Inflation affects everything from operational costs to investment strategies- Credit Quality:

Rising interest rates can lead to higher loan delinquency rates and defaults

. Banks need to increase their provisions for potential credit losses, impacting their

financial health and stability

Regional Variations

- United States: banks face higher funding costs due to intense competition for deposits and the

presence of money market funds - smaller banks are particularly affected, with deposit costs

rising more sharply compared to larger institutions - Europe: banks have managed to keep deposit costs relatively lower due to less competition

from money market funds - they still face challenges related to economic slowdowns and

regulatory changes post-Brexit - Asia-Pacific: banks with stronger economic growth, like India, may sustain higher rates but

are expected to generate stronger net interest income compared to their global peers

Deposit Competition

The competition for deposits has intensified, driven by higher interest rates and customer

expectations for better returns

Several Challenges of This:

- Rising Costs:

Cost of interest-bearing deposits has increased significantly, forcing banks to offer higher

rates to attract and retain customers

. This trend is expected to continue, even if central banks lower policy rates in the future

- Customer Behaviour:

Customers are more willing to switch banks in search of better yields, increasing the

competitive pressure on banks to offer attractive deposit rates

. This behaviour is facilitated by the ease of transferring funds between institutions

- Strategic Responses:

Diversifying their income sources, optimising their asset-liability mix, and enhancing

liquidity management practices

Investment in financial technology are crucial to improve efficiency and customer service

TECHNOLOGICAL ADVANCEMENTS AND DIGITAL TRANSFORMATION

Changes Are Reshaping How Banks: operate - engage with customers - manage risk

Key Areas of Focus Include The Adoption of

- Artificial Intelligence (A)) and Machine Learning (ML)

- Rise of Digital Banking

- Implementation of Advanced Cybersecurity Measures

Adoption of Artificial Intelligence (A) and Machine Learning (ML)

Benefits: Automating Tasks - Enhancing Customer Service - Improving Risk Management

. Key Applications: A)-Powered Customer Service - Fraud Detection and Prevention - Risk

Management and Credit Scoring

A)-Powered Customer Service - Chatbots and Virtual Assistants

- A)-driven chatbots, such as Bank of America's Erica, provide round-the-clock customer

support, handling inquiries ranging from balance checks to loan information - Use Natural Language Processing (NLP) to understand and respond to customer queries,

freeing up human agents for more complex tasks and improving customer satisfaction

A)-Powered Customer Service - Personalised Services

A) enables banks to offer personalised product recommendations and services by analysing

customer data and preferences

This leads to more targeted marketing campaigns and improving customer engagement

Fraud Detection and Prevention - Real-Time Monitoring

- A) systems can analyse vast amounts of transaction data to detect unusual patterns or

anomalies that may indicate fraudulent activity - These systems continuously learn from new data, allowing them to adapt to emerging threats

and provide a proactive defence against fraud

Fraud Detection and Prevention - Enhancing Security

A) improves effectiveness of cybersecurity measures by predicting and preventing cyberattacks

Monitor internal threats and suggest corrective actions, thereby preventing data breaches and

ensuring the security of customer information

Risk Management and Credit Scoring - Predictive Analysis

- Better-informed lending decisions and improving risk management

Risk Management and Credit Scoring - Automation of Risk Assessment

A) automates the risk assessment process, making it faster and more accurate

Useful in credit scoring and loan origination, where timely and precise evaluations are crucial

REGULATORY AND COMPLIANCE PRESSURES

Reasons for Regulation

Public Money - Backbone of The Modern Economy

Regulatory and Compliance Pressures

- The banking sector is under increasing regulatory scrutiny and must navigate a complex

landscape of evolving regulations - These pressures stem from the need to enhance financial stability, protect consumers, and

address emerging risks

Key Areas of Focus Include The Implementation of Basel Standards

Heightened Regulatory

Scrutiny - Post-Brexit Regulatory Landscape

Implementation of Basel 11) Standards

Basel ") is a comprehensive set of reforms developed by the Basel Committee on Banking

Supervision in response to the financial crisis of 2007-2009

The Reforms Aim To Strengthen The: Regulation - Supervision - Risk Management of Banks

. Key Components Include: Capital Requirements - Liquidity Requirements - Risk Management

Enhancements

Basel 3.1

- Are being implemented in phases, with full compliance expected by 2025

- Measurement of RWAs - banks' capital ratios more consistent and comparable

Post-Brexit Regulatory Landscape

- UK's Financial Services and Markets Bill: principle-based approach that regulators greater

responsibility and emphasising flexibility, competitiveness, and innovation - Prudential Regulation Authority (PRA): has published policy statements covering the

implementation of Basel 3.1 standards, reflecting adjustments based on industry feedback to

ensure proportionality and clarity in the new rules - EU VS UK Approaches:

UK: a principles-based approach, focusing on growth and international competitiveness

- EU: prioritise financial stability, market integrity, and investor protection

CUSTOMER EXPECTATIONS AND EXPERIENCE

Customer Expectations and Experience

Shift in customer expectations, driven by advancements in technology and changing consumer

behaviour

Modern Customers' Demands: Personalised - Seamless - Convenient Banking Experiences

. Buy Now Pay Later (a loan)

Key Aspects of Personalisation

- Data Utilisation:

Insights From Large Datasets: use advanced analytics to understand customer behaviour

Personalised Product Recommendations: tailored financial products for different customers

segments

Targeted Marketing Campaigns: A) and real-time data enhance marketing efforts

> Example: A)-driven financial product offerings

- Customer Profiles:

Robust Profiles: transaction history - social media activity - non-traditional data

Hyper-Personalised Experiences: enhanced customer satisfaction

Financial Inclusion: servicing traditionally underserved communities

- Real-Time Interactions:

A) and Real-Time Data: priority for proactive and intelligent interactions

Proactive Financial Advice: timely - relevant advice for customers

Issue Alerts: early warnings on potential financial issues

Benefits of Personalisation

- Increased Customer Retention:

Higher Customer Satisfaction: personalised services lead to loyalty

- Customer Loyalty: customers feel understood and valued

> Example: long-term customer relationships

- Cross-Selling Opportunities:

Understanding Customer Needs: effective cross-selling of products and services

- Increased Revenue: higher deposit rates - lower delinquency rates

- Enhanced Customer Experience:

Improved Interactions: relevant and meaningful interactions

- Higher Engagement: stronger emotional connection with the bank

> Example: personalised customer journey

OPERATIONAL AND STRATEGIC CHALLENGES

Operational and Strategic Challenges

Primarily Driven By: technological advancements - competition from fintech companies -

the need for robust cybersecurity measures

Higher Efficiency = Higher Profits

Key Cybersecurity Challenges

Data Breaches

Banks are prime targets for cybercriminals due to sensitive financial information they hold

Data breaches can result in significant financial losses, reputational damage, and

regulatory penalties

Advanced Persistent Threats (APTs)

Sophisticated, long-term cyberattacks aimed at stealing data or disrupting operations

Banks must invest in advanced threat detection & response capabilities to mitigate this risk

Ransomware Attacks

Where cybercriminals encrypt data and demand a reason for its release - are on the rise

Banks need to implement robust backup and recovery plans to minimise the risk of these

CrowdStrike Incident

Fortune 500 stand to lose $5 billion

Coding error causes Window services shut down (in July 2024)

Cybersecurity Measures

- A)-Driven Security:

A) and ML are used to enhance cybersecurity

Analyse data from previous threats and predict potential attacks, helping banks stay ahead

of cybercriminals by identifying vulnerabilities and implementing preventive measures

- Blockchain Technology:

Provides a secure, decentralized ledger of transactions

Improves security and transparency of financial transactions, especially for international

transactions

Reduces settlement times and eliminates the need for intermediaries

- Regulatory Compliance:

Banks must comply with strict cybersecurity regulations and guidelines, e.g. General Data

Protection Regulation (GDPR) & Payment Card Industry Data Security Standard (PCI DSS),

to ensures that banks implement necessary security measures to protect customer data

Key Areas of Competition From Non-Traditional Players (Fintech Companies and Tech Giants)

- Digital Payments: fintech companies have revolutionized digital payments, offering seamless

and convenient payment solutions

Can’t find what you’re looking for?

Explore more topics in the Algor library or create your own materials with AI.