Costs and Profits in Microeconomics: Production Factors and Cost Curves

Slides from University about Costs and Profits. The Pdf explores the fundamental concepts of costs and profits in microeconomics, defining profit as the difference between revenue and total costs. This Presentation, suitable for university-level Economics, analyzes production factors, their relation to time, and illustrates short and long-run cost curves, explaining economies and diseconomies of scale.

See more10 Pages

Unlock the full PDF for free

Sign up to get full access to the document and start transforming it with AI.

Preview

Costs and Profits Overview

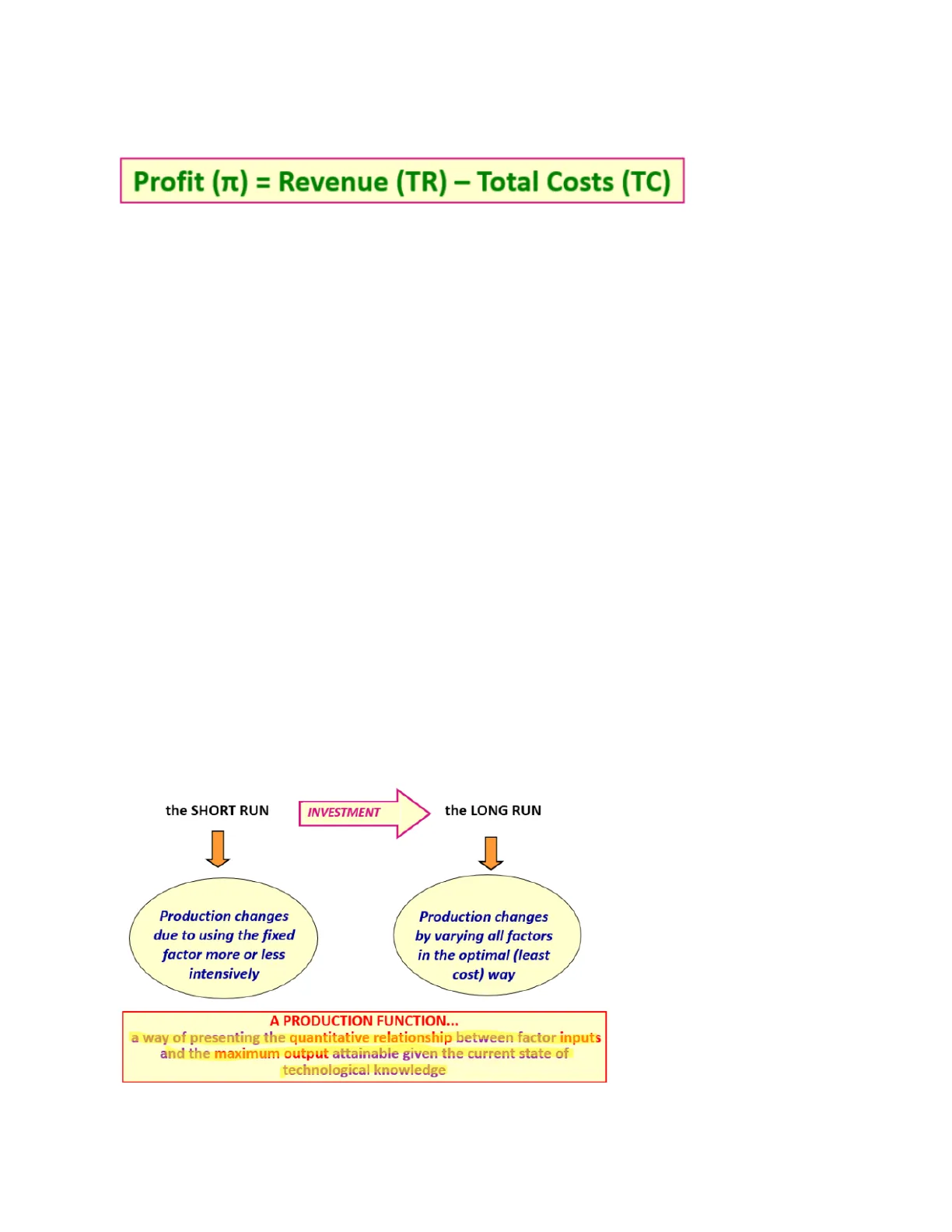

Profit (Tt) = Revenue (TR) - Total Costs (TC)

Costs helps a firm maximize its profitability in two ways:

- Technical efficiency: when a 'given' level of output is produced using the minimum

amount of inputs (avoiding waste) - 'optimal' level of production depends on both costs and market demand

conditions

To understand the costs first the production process needs to be understood which is what

generates a firm's costs

Factors of Production and Time

A firm can produce goods and services by combining the Four Factors of Production

- Firms have choices as how they are combined

- Different combinations of factors willl have different costs associated with them

Short Run vs. Long Run

- The short run

- Is the time of period over which a least one factor is fixed (often capital or land)

- The long run

- Is the time period over which all factors are variable (no such thing as fixed

factor of production)

- Is the time period over which all factors are variable (no such thing as fixed

the SHORT RUN

INVESTMENT

the LONG RUN

Production changes

due to using the fixed

factor more or less

intensively

Production changes

by varying all factors

in the optimal (least

cost) way

Production Function

A PRODUCTION FUNCTION ...

a way of presenting the quantitative relationship between factor inputs

and the maximum output attainable given the current state of

technological knowledge

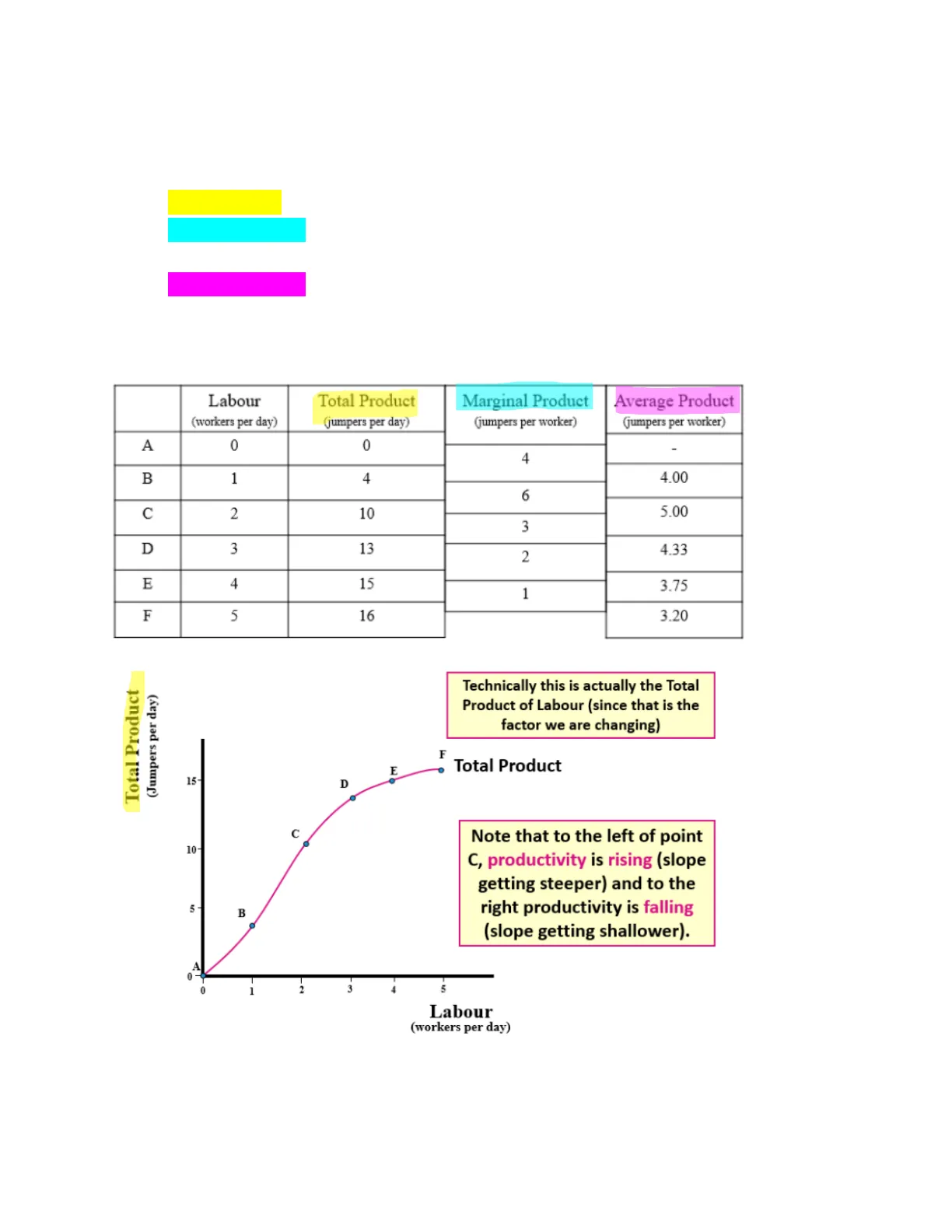

Definitions of Product Measures

- Total product: the total amount produced

- Marginal product: the change in total product resulting from one unit-increase in a

variable factor (in this case labour) - Average product: of an input in the total product divided by the quantity of the input

used- TOTAL PRODUCT / QUANTITY OF THE INPUT USED

Labour

(workers per day)

Total Product

(jumpers per day)

Marginal Product

(jumpers per worker)

Average Product

(jumpers per worker)

A

0

0

4

4.00

C

2

10

3

D

3

13

2

4.33

E

4

15

1

3.75

F

5

16

3.20

Total Product Curve Analysis

Total Product

(Jumpers per day)

Technically this is actually the Total

Product of Labour (since that is the

factor we are changing)

F

Total Product

E

15-

D

C

10-

5 -

B

Note that to the left of point

C, productivity is rising (slope

getting steeper) and to the

right productivity is falling

(slope getting shallower).

A

0

1

2

3

14

5

Labour

(workers per day)

-

B

1

4

6

5.00

Marginal Product Curve Analysis

Marginal Product

(Jumpers per person per day)

Note that Marginal Product is

also measured by the slope of

the Total Product curve

Technically this is actually

the Marginal Product of

Labour (since that is the

factor we are changing)

Marginal Product

0

Labour

(workers per day)

As a firm uses more of a variable input, with a given quantity of fixed inputs, there will come

a point when each additional unit of the variable factor will produce less extra output then

the previous unit.

This is what gives the MP curve its "bell" shape

Initially the MP of an additional worker exceeds the MP of the previous worker

- This occurs due to specialization/division of labour

- This is what we call increasing marginal return

At some point Diminishing Marginal returns sets in which is where the MP of an additional

worker is less than the MP of the previous worker

- More and more worrkers are using the same amount of machinery, so there is less

for the additional workers to do

Law of Diminishing Returns

Marginal Product

(Jumpers per person per day

Law of Diminishing Returns sets in

Increasing Marginal Returns

Diminishing Marginal Returns

Marginal Product

0

Labour

(workers per day)

Average Product and Marginal Product Relationship

Average product

Marginal Product

(Jumpers per person per day)

In essence this behaves like any other average variable

Note that the MP curve always intersects

the AP curve at its highest point

Average Product

Marginal Product

Labour

(workers per day)

From Production to Costs

We describe the relationship between output and costs by using three concepts

- Total costs are the cost of all the factors of production the firm uses

- Marginal cost is the change in Total Cost from one unit-increases in output

- Average cost is the cost per unit of output

Short-Run Cost Analysis

The impact of short-run analysis

In the short run some inputs are fixed. Their costs are therefore fixed

Other inputs can be varied. Their costs are therefore variable.

- Total fixed cost is the cost of fixed inputs

- Total variable cost is the cost of variable inputs

- Total cost is the sum of both

TC = TFC +TVC

If we assume capital costs are £25, and it costs £25 to employ

a unit of labour, we can construct the following:

Labour

(workers per day)

Output

(jumpers per day)

TFC

(£ per day)

TVC

(£ per day)

TC

(£ per day)

0

0

25

0

25

1

4

25

25

50

2

10

25

50

75

3

13

25

75

100

4

15

25

100

125

5

16

25

125

150

Total Cost Curve

(pounds per day)

TC

Cost

TVC

1

TFC

İ

0

0

Output

(jumpers per day)

Average and Marginal Costs

Average cost and marginal costs

- Average cost is the cost per unit of production

- Average fixed cost

- Average variable cost

- Average total cost

TC = TFC + TVC

Q

Q

- Marginal cost is the total cost of production one extra unit of output:

MC = ATC / AQ

Marginal Cost and Average Cost Curves

MARGINAL COST AND AVERAGE COSTS

Costs (£)

MC

ATC

Note minimum points

for ATC & AVC, and

their intersection with

AVC

MC curve!

1

1

AFC

Output (Q)

- Marginal cost and ATC are 'U-shaped' because initially there are economies due to

specialization but ultimately the diminishing returns arrive - The AVC curve gets closer and closer to ATC because FC are being spread over

increasing amounts of output

Long Run Cost Analysis

The long run

- All factors of production are variable

- The object is to minisme production costs for a given amount of output

- The main focus is upon altering the size of the capital stock to achieve the least cost

means of production- Just as we had diminishing returns to labour, we also have diminishing returns to

capital (when labour is fixed) - Need to find the optimal blend of the factor of production

- Just as we had diminishing returns to labour, we also have diminishing returns to

Optimal Factory Size

FROM PRODUCTION TO COSTS

Costs (£)

What is the Optimal factory size?

If Output 0-Q1, then Factory 1

If Output is Q1-Q2, then Factory 2

If Output is > Q2, then Factory 3

SRATC2

SRATC1

SRATC3

With larger factories,

there are higher fixed

costs thus SRATC are

minimised at higher levels

of output

0

Q1

Q2

Quantity (Q)

Short Run to Long Run Average Cost

FROM SR TO LR

Costs (£)

AC in the Long Run is made up from

a 'family' of SR-ATC curves!

SRATC2

SRATC3

SRATC1

LRAC

0

Quantity (Q)

Theoretically there are an infinite number of factory sizes

Costs (£)

SRATC

SRATC

SRATC

SRATC

SRATC

LRAC

0

Quantity (Q)

- The long run is just a series of short runs as every short run cost can be turned into

long run - The LRAC provides a description of the lowest cost method of producing any given

amount of output - SRATC curves are tangential to LRAC curve

Why LR-AC is U-Shaped

WHY IS LR-AC 'U' SHAPED?

Costs (£)

Increasing Returns to Scale LRAC V

Constant Returns to Scale LRAC-

Decreasing Returns to Scale LRACÎ

IRS

CRS

DRS

LRAC

Economies of

Scale

Diseconomies of Scale

0

Minimum Efficient

Scale (MES)

Quantity (Q)

Economies and Diseconomies of Scale

Economies of scale and diseconomies of scale

- Economies of scale are feature of a firms technology that lead to falling long run

average cost as production increases- Specialization of labour and capital

- Bulk buying

- Indivisibility

- Greater efficiency of large machines

- The container principle

- Organizational efficiencies

- Finanancial economies

- Economies of scope (variety not volume)

- External economies

- Diseconomies of scale are the features of a firm's technology that lead to rising

long run average cost as production increases- Complex management and organization structures

Can’t find what you’re looking for?

Explore more topics in the Algor library or create your own materials with AI.