Exchange Traded Funds, structure, types, and digital assets

Slides about Exchange Traded Funds. The Pdf explores ETFs, their structure, types, and differences from mutual funds, covering concepts like backwardation and contango. The Presentation, suitable for University Economics students, also delves into Digital Assets, blockchain, and consensus mechanisms like Proof of Work and Proof of Stake.

See more40 Pages

Unlock the full PDF for free

Sign up to get full access to the document and start transforming it with AI.

Preview

EXCHANGE TRADED FUNDS

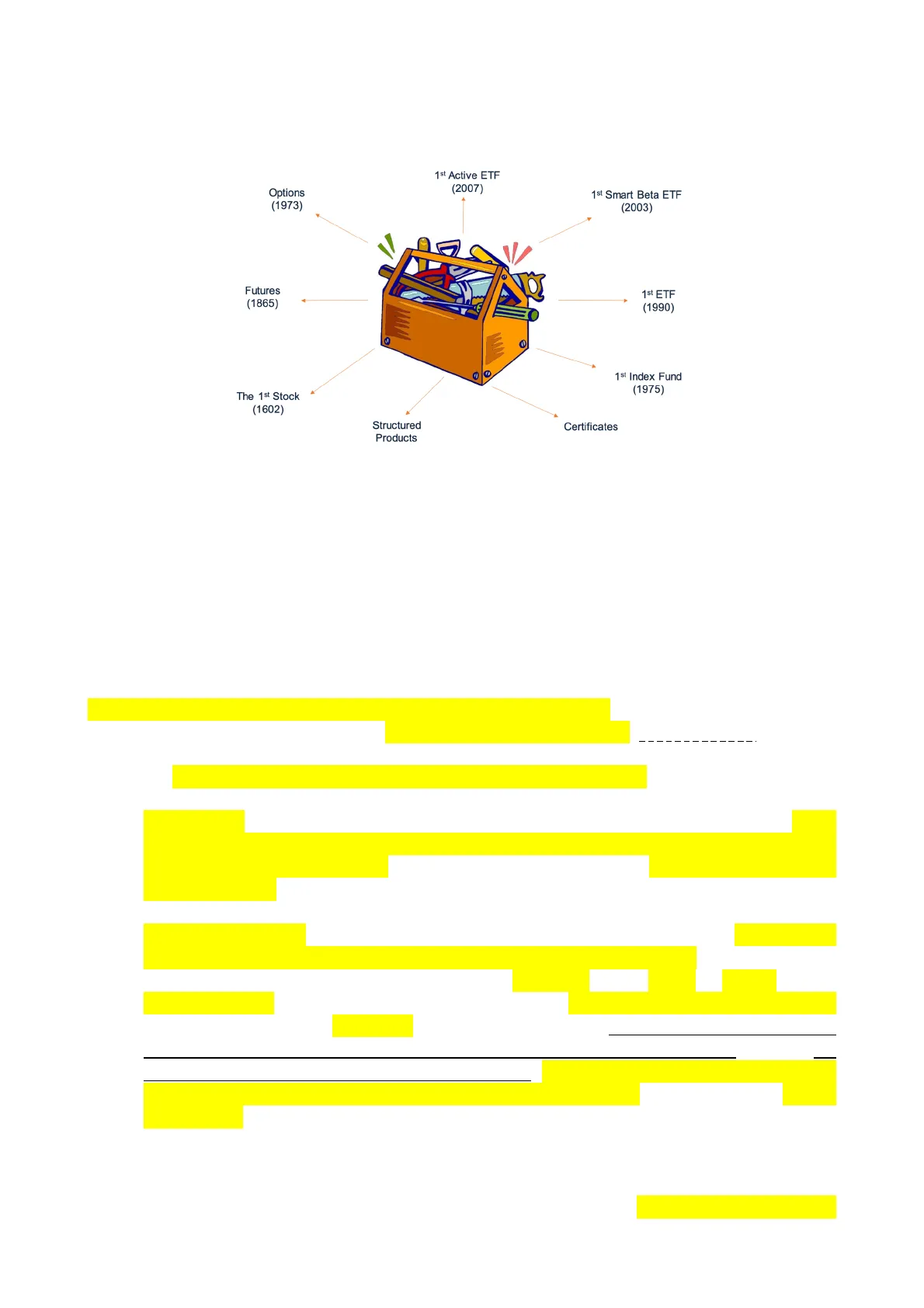

1st Active ETF (2007) Options (1973) 1 st Smart Beta ETF (2003) Futures (1865) 1 st ETF (1990) C 1 st Index Fund (1975) The 1st Stock (1602) Structured Products Certificates

The world's first ETF was created in Canada in 1990, transforming the investment landscape and offering the advantages of pooled investing and trading flexibility. In Italy the first ETF was launched in 2002 by Borsa Italiana.

ETF STRUCTURE

WHAT IS AN ETF

An ETF is an open-ended fund which is traded in the stock exchange Similarly, to a mutual fund, ETFs can be considered a basket of securities (stocks or bonds).

ETF can be CLASSIFIED based on their MANAGEMENT METHODOLOGY into three main categories:

- Active ETFs: These involve a more hands-on portfolio management approach. The management team makes active investment decisions by selecting and regularly adjusting the securities within the fund to try and outperform a benchmark or achieve superior returns ("seeking alpha"). These funds entail greater managerial discretion and more direct human involvement in security selection compared to passive ETFs.

- Index ETFs (Passive): Index ETFs, also known as passive ETFs, aim to replicate the performance of a specific benchmark index (such as the S&P 500, FTSE 100, etc.). These funds simply track the underlying index's performance, seeking to closely mirror its returns.

- Smart Beta ETFs: Smart beta ETFs employ investment strategies that lie between passive market-based investing and active portfolio management. These ETFs seek to enhance performance relative to a traditional benchmark index by using specific rules or filters for selecting and weighting securities within the fund. Smart beta strategies typically involve weighting based on specific factors (such as value, size, volatility, etc.) rather than market capitalization.

In summary, active ETFs involve active portfolio management, index ETFs replicate the performance of a specific index without active interventions, while smart beta ETFs aim to improve performance relative to a benchmark index using strategies based on specific factors. The choice between these2 categories depends on an investor's preferences regarding investment strategy, risk, and return objectives.

ETF FEATURES AND MUTUAL FUND DIFFERENCES

ETFs follows the same regulation of mutual funds in Europe. Their dividends can be distributed or accumulated. Similarly, to mutual funds, Exchange-Traded Funds (ETFs) are diversified instruments as they allow investors to own a portion of a diversified portfolio composed of a series of securities or assets. This offers a reduction in the specific risk of a single security or sector. In terms of costs, there are no entry, exit, or performance fees; the only costs are the management fees (TER - Total Expense Ratio): annual expenses covering the fund's management costs, including the fund manager's fees, operational, administrative, and distribution costs. The asset manager's responsibility is over the invested asset against the performance objective. Regarding trading, while mutual funds are bought and sold directly by the management company at the net asset value calculated at the closing of the daily market, ETFs are traded like stocks during market hours, and their price may fluctuate based on supply and demand (= ETFs are traded and not subscribed).

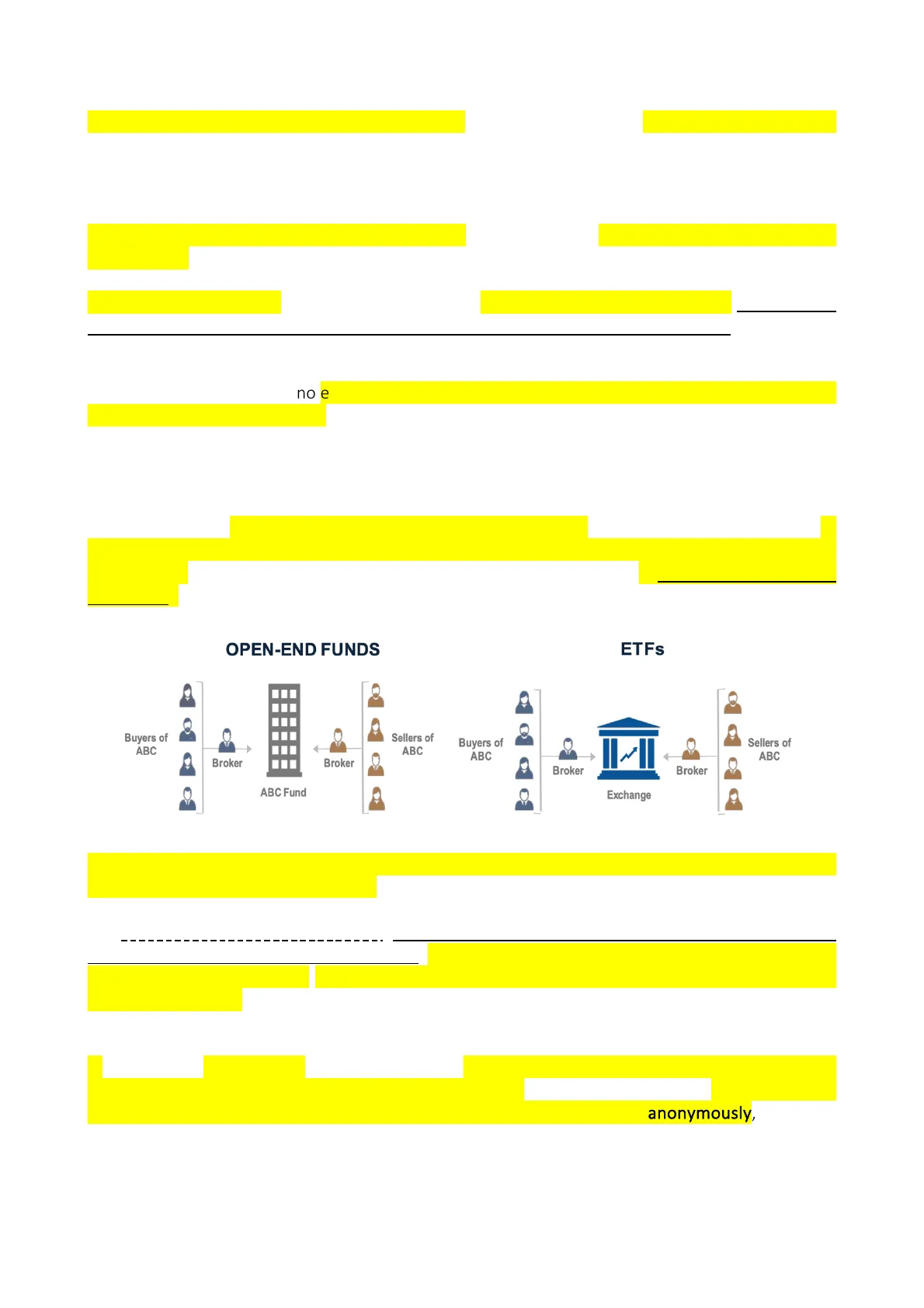

OPEN-END FUNDS

Buyers of ABC Sellers of ABC Broker Broker ABC Fund

ETFs

Buyers of ABC Sellers of ABC Broker Broker Exchange

ETF can be priced by market price, NAV and iNAV (while NAV takes into consideration end-of-the- day data, iNAV considers intraday data). The iNAV or Indicative Net Asset Value. Calculated on a minute-by-minute basis by ETF custodians and Third-party vendors such as Bloomberg. INAV is calculated by considering the market prices of individual holdings in a fund. iNAV enables investors to receive an up-to-the-minute indication of what an ETF is worth that can be used to check their own calculations or by comparing the iNAV with bid-ask spreads, see whether an ETF is being priced fairly in the market. In the case of mutual funds, the fund issuer or management company maintains records of the investors who hold shares in the fund. However, with ETFs, the situation is different. When investors buy or sell ETF shares on the stock exchange, their transactions occur anonymously like stock transactions. The ETF issuer generally doesn't track or have information about the specific individuals buying or selling ETF shares on the secondary market.3 ETFs are generally more transparent compared to mutual funds as they disclose the list of securities they are composed of in real-time or more frequently than mutual funds, which typically disclose their holdings less frequently (usually quarterly). While mutual funds may require a minimum investment amount, ETFs can be purchased in any quantity, even a single share.

OPEN-END FUNDS vs ETFs

OPEN-END FUNDS Transactions executed after exchange closure Price defined on securities last price (NAV). Transactions are blind Taxation run by the fund Accumulation plan

ETFs Transactions operates during the whole exchange hours. Real time exchange price Investors can set trading price limits Taxation run by the broker Accumulation plan set by the broker Last NAV Mi iNAV

In open end funds, transactions are blind: we know the price at which we subscribe a fund just the day after the processing of the subscription, or in 2 days, while with ETF we know immediately the price at which we buy because it's quicker.

Features Comparison

Features Mutual fund ETF Stock Diversification x Transparency X x Exchange trading × Intraday Trading X Daily NAV × Management Fees ×

PASSIVE ETFS (CAP WEIGHTED)

The ETF manager is supposed to track the index performance as close as possible. These ETFs do not seek market alpha but rely solely on beta for their performance. The beta is a measure of volatility showing how volatile stocks or funds are relative to their benchmark indices. A benchmark has a fixed beta of 1. A stock or fund with a beta of more than 1 moves up and down more than the market, while the value of a stock or fund with a beta of less than1 will fluctuate less than the market.4 Management fees are usually lower because there are no entry and exit costs, no distribution costs, and no financial analysis costs because it is simply replicating an index. Passive ETFs are easy to understand and to track, as they follow the index.

Benchmark Index Performance

Benchmark Index Performance Passive ETF Time

Originally, ETF have been designed to be passive, which means to replicate an index. The passive ETF track the performance of the index; the capitalization weighted index is an index where the investible universe is the largest stock in the market. An index changes its composition overtime. It's a useful tool to answer simple questions, like for example the market is going. Passive ETFs are generally cheaper than funds, indeed, for example global ETF average cost is 0,21% while Italian investment fund cost is 1,72%. Overtime, cost matters and it weights a lot in the returns. In case ETF and fund has the same performance, the ETF cost less.

HOW IS AN ETF BUILT?

Let's image the FTSE 100 index. It's made of 100 stocks; we know the components and the weight (they are public). The ETF will track the index, and so it will buy for the exact same stock in the same amount. With one single transaction, you buy all the ETFs. In this way we pass from a not investible index to an investible product available to everyone. The construction of an Exchange-Traded Fund (ETF) that tracks the FTSE 100, a British stock index, can be divided into several steps:

- Selection of the benchmark index (FTSE 100): The ETF is designed to track a specific index, III LIIS Case, We TTJE 100. merTL 100 is a market-capitalization-weighted index representing thaton 100 commaning listed on the London Stock Exchange.

- Structuring the basket : The ETF issuer, in collaboration with FTSE Russell (the entity managing the FTSE 100), determines which stocks should be included in the ETF based on the index's weightings.5

- Weighting of Stocks in the Basket: The stocks in the ETF's basket are weighted based on market capitalization. This means that companies with a larger market capitalization will have a greater weight in the ETF. This weighting replicates the structure of the FTSE 100 index.

- Creation of the Creation Unit: A measure used in the ETF Primary Market where ETFs are created and redeemed by Market Participants. A creation unit is a block of thousands of shares of an ETF and is the smallest block of shares that can normally be bought or sold by market participants. The size of creation units may vary between funds. Creation unit transaction take place in kind (stocks) or in cash.

- Exchange Trading: The ETF is then listed and traded on the stock exchange like an ordinary stock. Investors can buy or sell ETF shares at any time during market trading hours.

- Arbitrage Activities: Arbitrageurs and market makers play a key role in maintaining the ETF's price in line with its net asset value (NAV). If the ETF is traded at a significantly different price from its NAV, arbitrageurs can exploit these differences to earn profits through arbitrage transactions.

- Fund Management: The ETF issuer is responsible for fund management, which includes periodically rebalancing the portfolio to ensure it continues to faithfully reflect the performance of the FTSE 100 index.

ETFS: SUBSCRIPTION AND REDEMPTION PROCESS

The ETF is traded in two primary markets: the primary market and the secondary market.

IN THE PRIMARY MARKET

riscattate In the primary market, new shares of an ETF are created or redeemed. This process directly involves the ETF issuer and the so-called "Authorized Participants." Authorized Participants are often large financial institutions, such as banks or brokers, authorized to transact directly with the ETF issuer. During the creation of new shares (creation of creation units), Authorized Participants provide the ETF issuer with a block of the underlying assets of the ETF in exchange for new ETF shares. In the case of redemption, the operation occurs in reverse, with Authorized Participants returning the ETF shares in exchange for the underlying assets. This process occurs in-kind, meaning the creation unit is exchanged for a basket of physical assets (stocks, bonds, etc.) or in cash, depending on the ETF's rules.

IN THE SECONDARY MARKET

The secondary market is where most ETF transactions take place. In this market, investors buy and sell ETF shares among themselves, much like they would with shares of any company. ETFs are listed and traded on stock exchanges like ordinary stocks. The liquidity of the ETF secondary market is facilitated by so-called "market makers." These are specialized firms that provide liquidity to the market by maintaining an inventory of ETF shares and being ready to buy or sell when investors want to trade. In summary, in the primary market, new ETF shares are created or redeemed through direct transactions with the issuer and Authorized Participants, while in the secondary market, investors exchange ETF shares among themselves on stock exchanges, facilitated by market makers. Market price ~ iNAV (there is no premium/discount) ETF liquidity ~ index securities liquidity Exchange volumes # real liquidity.

Can’t find what you’re looking for?

Explore more topics in the Algor library or create your own materials with AI.