AG309 Client Acceptance and Quality Control, University of Strathclyde Business School

Slides from University of Strathclyde Business School about AG309 Week 10 Client Acceptance and Quality Control. The Pdf provides a clear overview of procedures and responsibilities for university students of Economics, covering the IFAC Code, engagement letters, and audit files.

See more30 Pages

Unlock the full PDF for free

Sign up to get full access to the document and start transforming it with AI.

Preview

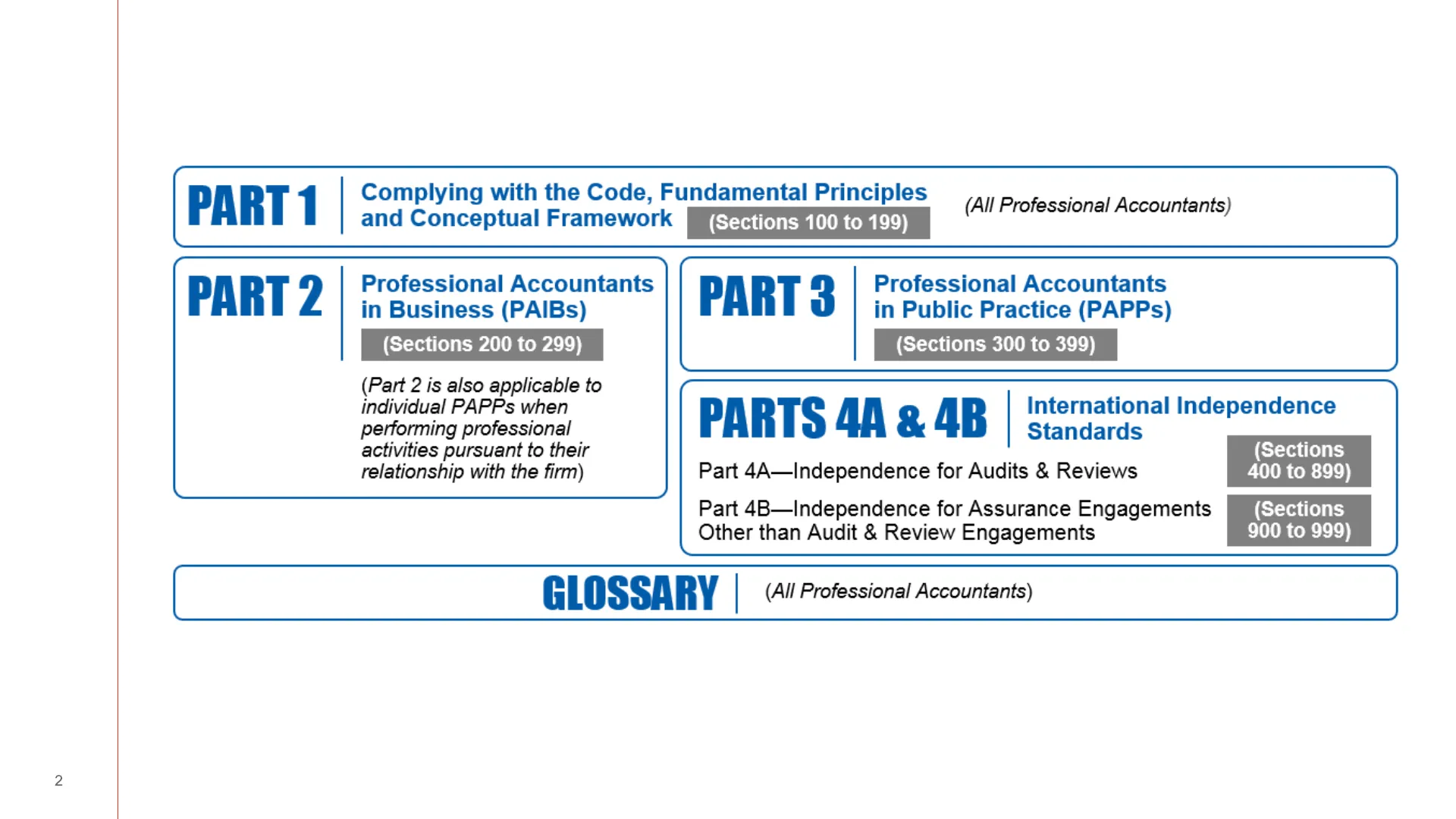

IFAC Code Structure

STRATHCLYDE BUSINESS SCHOOL IFAC Code PART 1 Complying with the Code, Fundamental Principles and Conceptual Framework (Sections 100 to 199) (All Professional Accountants)

PART 2 Professional Accountants in Business (PAIBs) (Sections 200 to 299) (Part 2 is also applicable to individual PAPPs when performing professional activities pursuant to their relationship with the firm)

PART 3 Professional Accountants in Public Practice (PAPPs) (Sections 300 to 399)

PARTS 4A & 4B International Independence Standards (Sections 400 to 899) Part 4A-Independence for Audits & Reviews Part 4B-Independence for Assurance Engagements Other than Audit & Review Engagements (Sections 900 to 999)

GLOSSARY (All Professional Accountants) 2X

FRC Ethical Standards Code - 2024

STRATHCLYDE BUSINESS SCHOOL FRC Ethical Standards Code - 2024 UK standards based on IAASB/IFAC code. Audit firms registered in the UK must comply with the ethical standards set out in this code. https://media.frc.org.uk/documents/Revised Ethical Standard 2 024.pdf Overarching principles of Integrity, Objectivity and Independence. Particular rules applicable especially to PIEs. 3X

Threats to Objectivity and Independence

- Self-interest

- Self-review

- Advocacy

- Familiarity

- Intimidation SSAFI + Management threat Variety of safeguards that can be put in place to mitigate. 4X

Potential New Audit Clients

STRATHCLYDE BUSINESS SCHOOL Potential New Audit Clients Free to refuse to act for any client. Must turn down if: · You are not a qualified auditor · There are unmitigable independence issues The process of determining whether to accept a client and the administration of onboarding/accepting the client is know as 'Client Acceptance', 5X

Independence Considerations for New Clients

STRATHCLYDE BUSINESS SCHOOL Independence When a potential new client is being considered, staff within the audit firm should be contacted and questioned to consider if there is any independence issues. It is also required that the firm continue to request updates from their staff to ensure that any independence issues are identified and mitigated as appropriate. However some threats to independence can never be acceptably mitigated against. 6X

Further Issues to Consider for Client Acceptance

STRATHCLYDE BUSINESS SCHOOL Further Issues to Consider Resources Do you have the resources (mainly personnel) to perform the audit in the required timetable? Expertise Do you have the required expertise to carry out the audit to be able to get reasonable assurance with which to provide your opinion. Fees Will the fee be sufficient to allow you to do a good quality audit? Reputation Is this a client you wish to be associated with? 7X

Risk Assessment for Client Acceptance

STRATHCLYDE BUSINESS SCHOOL Risk Assessment Before accepting a client the firm should undertake a risk assessment on that client. What should be considered? Risk Assessments should be clearly documented and ongoing. 8X

Client Acceptance and Identification Procedures

STRATHCLYDE BUSINESS SCHOOL Client Acceptance Upon accepting a client the firm is required to undertake identification procedures (KYC/CDD) to ensure: . The client (including any key management in a company) are who they say they are · Sources of funds etc. are genuine Why? 9X

Client Acceptance - Sources of Information

STRATHCLYDE BUSINESS SCHOOL Client Acceptance - Sources of Info Where will you access all of the information needed for your KYC/CDD? https://www.accaglobal.com/uk/en/technical-activities/technical-resources-search/2020/june/client- risk-assessment-kyc.html 10X

Professional Etiquette and Clearance

STRATHCLYDE BUSINESS SCHOOL Professional Etiquette/Clearance Ask clients permission to contact previous auditor: · Aware of any reasons why we should not accept · Requesting copies of prior year working papers · Provision of any other relevant information Previous auditor on receipt should ask client for permission to respond. 11X

Letter of Engagement

STRATHCLYDE BUSINESS SCHOOL Letter of Engagement The letter of engagement (LOE) is essentially a contract between the auditor and the client. Sets out the relationship between the client and the auditor. Required both by law, and by ISA 210. Includes: · Terms of audit including fees · Respective responsibilities of client and auditor · Standards used 12X

Tailoring the Letter of Engagement

STRATHCLYDE BUSINESS SCHOOL Letter of Engagement Each firm will have a standard letter of engagement. Tailored to each client for items such as: · Groups - included entities · Overseas branches - plan to deal with · Internal auditors - use of and/or relationship 13X

Signing the Letter of Engagement

STRATHCLYDE BUSINESS SCHOOL Letter of Engagement 2 copies signed and sent by auditor to client. Client should sign both and return 1 copy to auditor. No audit work should commence until the auditor has received a signed letter of engagement. 14X

When to Issue a Letter of Engagement

STRATHCLYDE BUSINESS SCHOOL Letter of Engagement An LOE should be issued when: An auditor first acts for a client A change in scope e.g. a new company in the group needing audited A change in circumstances e.g. a lot of firms recently re-issued engagement letters to account for GDPR data protection changes 15X

Engagement Partner Responsibilities

STRATHCLYDE BUSINESS SCHOOL Engagement Partner Each engagement should have an engagement partner they are the partner responsible for that engagement. The engagement partner's role is clarified in ISA 200, broadly speaking they are there to ensure that the audit is carried out correctly, e.g .: · Appropriate staff are allocated to the job and supervised. · Staff appropriately briefed as to nature of work and audit plan. . All audit work and conclusions appropriately documented. . All audit work is appropriately reviewed including sign offs. 16X

Audit Files Management

STRATHCLYDE BUSINESS SCHOOL Audit Files Should maintain a Permanent File for every client (either in hard or electronic format). The contents discussed further next semester but should contain permanent information on the client (e.g. previous approved financial statements, title deeds for property, LOE, client ID documents, and a copy of the resolution from the company appointing them as auditors should be maintained on this file.) Current Audit File - a file for each year of audit containing all working papers. 17X

Audit Quality Importance

STRATHCLYDE BUSINESS SCHOOL Audit Quality As you've seen already the auditing profession is extremely highly regulated and that the audit opinion is relied upon to a great extent by many parties. Clear requirement for the firm to ensure that its audits are of sufficient quality. Have to ensure that enough evidence is gathered and documented. 'If it's not on file, it didn't happen!' 18X

Audit Quality Reviews

STRATHCLYDE BUSINESS SCHOOL Audit Quality Reviews Public Interest Entities require a "Hot" review. The means that they are reviewed by an independent partner within the firm while the audit is still ongoing and before the audit report is issued. Additionally the FRC must inspect PIE auditors at least once every three years. "Cold" reviews are completed after an audit is completed. In general the firm will select a range of clients each year, an independent partner or other individual will review the file. In some cases a completely independent third party will be brought in to review the file. 19X

Results of Audit Quality Reviews

STRATHCLYDE BUSINESS SCHOOL Results of both "hot" and "cold" reviews will be considered by the firm. The resulting actions could include: · Changes to firms' procedures · New training rules/procedures · Matters to be discussed with specific members of staff "Hot" reviews may also dictate that further procedures are carried out prior to the opinion being given. 20X

Audit Reform Developments

STRATHCLYDE BUSINESS SCHOOL Audit Reform ... coming thick and fast Kingman Review 2018 (FRC review) and Brydon Review 2019 (Audit Quality) recommendations. BEIS 2021 paper - 'Restoring trust in audit and corporate governance' New PIE definition - 750:750 rule (e'ees: Turnover) + OEPIs https://www.bdo.co.uk/en-gb/insights/industries/professional-services/pies-oepis-and-restoring-trust-in-audit-and-corporate-governance Audit firm eligibility - Registered auditors must hold enough votes to make the decisions within a firm from 1 Oct 24 but 6m transition to 1 Apr 25. https://www.icas.com/regulation/regulatory-monitoring/changes-to-the-audit-regulations-eligibility 21X

Case Study: Bryn and Mackenzie LLP

STRATHCLYDE BUSINESS SCHOOL Case Study Bryn and Mackenzie LLP ('B&M') are a small accountancy firm based on the outskirts of Glasgow. Their existing clients are primarily small local businesses. They have 2 partners, 3 members of qualified staff and 5 students/ assistants. One of the partners' nephew, CEO of CWI Group, approached B&M looking for a new auditor for their Dec year end financials. CWI Group are a large listed insurance company who primarily carry out re-insurance of commercial debt instruments based in the off-shore Eurobond markets with activities in 16 EU countries. They have a turnover of £1.4bn and 9,000 members of staff. They are expecting the annual fee to come in around £15,000. 22X

Case Study Requirement

STRATHCLYDE BUSINESS SCHOOL Case Study - Requirement Outline and discuss the key considerations for Bryn and Mackenzie LLP in deciding whether to accept the work as auditor. (15 Marks) 23X

Case Study Approach

STRATHCLYDE BUSINESS SCHOOL Case Study - Approach You'll need to attend lecture to find out! 24X

Summary of Client Acceptance and Audit Quality

STRATHCLYDE BUSINESS SCHOOL Summary (you should be able to) · Describe the procedures for accepting a client . Describe the rules for client acceptance . Describe the risk of accepting a client . Describe the importance of ensuring quality of an audit . Describe the policies to ensure an audit is of sufficient quality 25X

Past Papers and Audit Report Coverage

STRATHCLYDE BUSINESS SCHOOL Past Papers . 2 past papers with solutions are on Myplace. Bear in mind different examiner last year. . Please remember the audit report is now covered in AG308 not this course. 26X

Tomorrow's Tutorial Preparation

STRATHCLYDE BUSINESS SCHOOL Tomorrow's tutorial Bring prepared answer to Question 1 You will be considering what mark you would achieve. Important to consider incorporating advice from today's assignment debrief. 27X

Further Work Resources

STRATHCLYDE BUSINESS SCHOOL Further work PDF AG309 Marking Guide PDF GUIDANCE ON MARKING ASSESSMENTS Which person to use in academic/professional writing XLS ACCA KYC Checklist PDF PWC FAQ on PIE Audit Quality 28

Can’t find what you’re looking for?

Explore more topics in the Algor library or create your own materials with AI.